2 February 2011 Do I Do Baidu?

BAGAKOAA 2 February 2011 Do I Do Baidu?

BIDI Baidu, Inc. provides Chinese and Japanese language Internet search services. Its search services enable users to find relevant information online, including Web pages, news, images, multimedia files, and blogs through the links provided on its Websites. If that description sounds familiar, that is because the business model is almost identical to GOOG Google Inc. In fact BIDU got a huge boost and a real solid foundation when GOOG chose to back step a bit in China. Before and since BIDU has been white hot. So that means we all lost a chance to get into the Chinese version of Google. Darn. BIDU is way too expensive with crazy P/E ratios. The current is 98 and forward looking is 50. When the S & P 500 is about 15-16, you gotta be crazy. Forget about it. Even the chart looks to hot to handle.

Well actually it is two charts One is of BIDU and one is of GOOG selling in the same price range for about the same length of time? Can you tell which is which? That is my point. There was huge jump on huge volume and this is a good thing. GOOG had many days like this early on. Today Google trades above $600 a share.

Well actually it is two charts One is of BIDU and one is of GOOG selling in the same price range for about the same length of time? Can you tell which is which? That is my point. There was huge jump on huge volume and this is a good thing. GOOG had many days like this early on. Today Google trades above $600 a share.

DO YOUR HOMEWORK. BIDU might be the next Google. $1,000 bucks in Google in 2004 (about the time its stock tracked BIDU) would be worth $5,545. The end point here is to not let the P/E ratio and current price scare you if you think the stock has legs.

IBD loves the stock and rates it a 98. Average earnings growth for the last three quarters is 139%. Year on year for the latest quarter is 109%. They beat expectations (BIG Expectations) by 13%. They have had 4 years of consecutive earnings growth and that was competing with Google. Google is all but gone from the market. It is performing in the top 5% of all stocks measured by IBD. It accumulating is neutral at the moment, but that might be because a lot of the big players (hedge fund, insurance companies etc,) were in and had to take some profit in December. If we see a few more days like Feb 1 you’ll see the accum/dist rating improve. 22 million shares were traded on Tuesday. Lost of new big traders. That’s a good thing. Let’s keep it close on a watch list.

Turning Over Some Stone

I have to admit we were tickled today to have one of our readers ask about a stock they were looking at. We were tickled as we admire this person’s knowledge and experience in the industry of financial advising. It was quite flattering. Thank you Doug.

The request was to kick the tires on RST Rosetta Stone Inc. which provides technology-based language learning solutions worldwide. The company develops, markets, and sells language learning solutions, such as software, online services, and audio practice tools primarily under the Rosetta Stone brand name. It offers self-study language learning solutions in approximately 31 languages. The company's approach, called Dynamic Immersion, eliminates translation and grammar explanation and is designed to leverage the natural language learning ability that children use to learn their native language. It also provides Rosetta Stone TOTALe, an online language learning solution that integrates its online courses with coach-led practice sessions, fun and engaging language games, interaction with native speakers, and live support from customer service agents. In addition, the company offers an online peer-to-peer practice environment called SharedTalk, at www.sharedtalk.com, where registered language learners meet for language exchange to practice their foreign language skills. It primarily serves individuals, home school parents, educational institutions, armed forces, government agencies, corporations, and not-for-profit institutions. The company sells its products through direct sales channels, including its call centers, Web sites, institutional sales force, kiosks, and certain retailers, as well as through the sale of CD-ROM's and on line subscriptions. Rosetta Stone Inc. is headquartered in Arlington, Virginia.

WE DO NOT OWN THE STOCK. We did have it on a watch list back in August, but never got a good entry point and forgot about it. Let’s look at the fundies first.

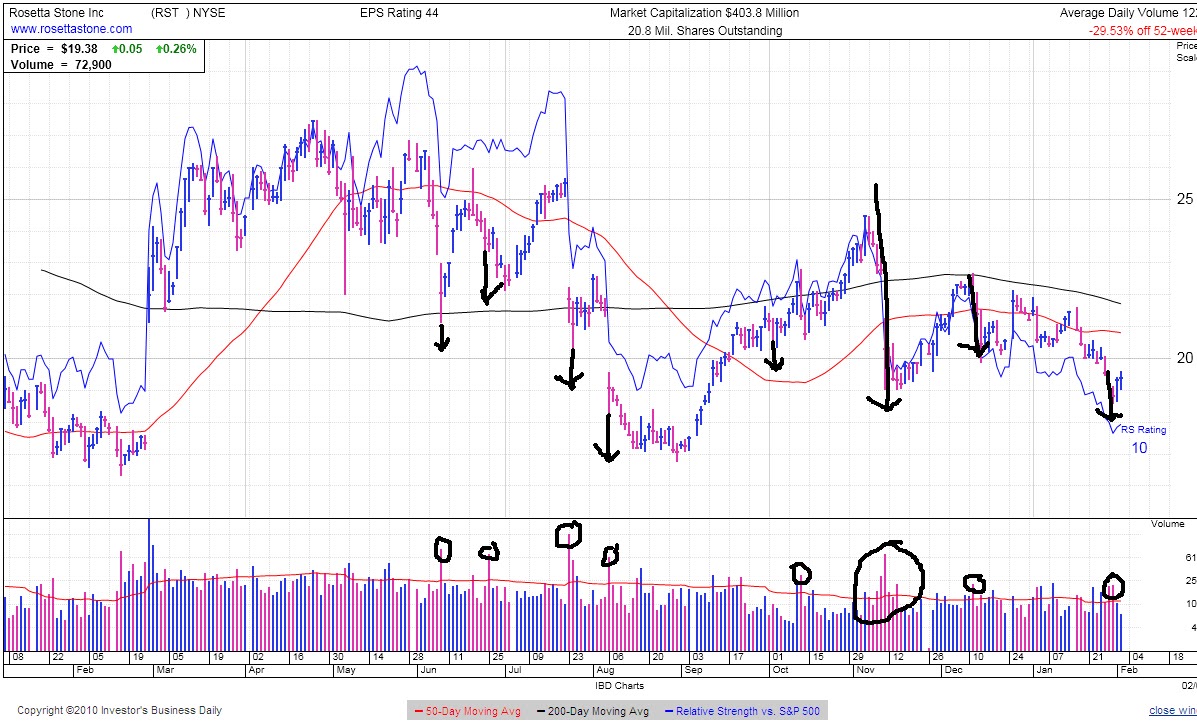

For the positive, they and analysts are looking for a 39% increase in earnings this year. They have about 5 bucks a share cash and decent cash flow. Institutional ownership seems to be slipping a bit. There are some target prices at 22 a share creating a fairly good margin of safety as the stock closed today at $19.38. On the down side, earnings did drop this year from last. The stock is trading below its 20, 50 and 100 day level. Considering the uptrend the market has had since August-September, RST seems to be going against the grain and seeking lower lows. Below is a chart that demonstrates is. Every singe volume day above the daily average has been a down day. As you know, in order to break over the average volume it takes institutional monies. This is also illustrated with the institutional ownership report we borrowed from Morningstar. You cans see the big money trends and they ain’t that pretty.

IBD does not like the pick. It has a 14 out of 99 overall rating on the equity. Most of the redflags include the sector rating which is educational software and is listed 116 out of 197 sectors. Most of the EPSG (Earnings per Share Growth) numbers were not impressive. It is 30% off its 52 week high and IBD likes stocks to at or near their 52 week high. The real negative for me is the IBD Accum/Dist rating. It is a D- which means this is being dumped. Being dumped in an upward market is not a good sign. Now let’s go to the SEC Filings and see if the CEO and CFO can tell why they are struggling.

In looking at the Nov 10Q filing, there are no surprises there and no real explanation other than 43% revenue comes directly from consumers and 30% comes from government and schools. Although it does not say it, the product is truly discretionary to the 43% base of consumers. In this day and age there are free and less expensive on line language learning aides and travel is just now beginning to recover. And as far as sales to the government and schools well good luck with that and be real careful of the accounts receivable. California is paying vendors with IOUs.

In a nutshell Rosetta has a great brand and plenty of opportunity. They generate less than 10 % of their revenue outside the US which leaves a lot of opportunity for growth, but they are not seeing it yet. They are well positioned in the largest brick and mortar and on line retailers in the world. That 30 % government business is leading to more international take up with other countries governments. The product itself is very effective and they have some proprietary technology with widens the competitive moat. All that said, we would wait until we see a reversal of institutional monies. RST needs a good quarter or two of earnings growth and few MF or Hedge funds to take notice and start accumulating. Until that happens, you are trying to catch a falling knife.

What happened today.

Now what actually did happened today in the market? We are batting about 60% on our data points and earnings calls this week which gives us some bragging rites. Snow Day In Manhattan. Ok they did not close banks and schools, but wicked weather made it hard to get buys and sellers together so volume was light and the number went sideways. The good news is we are still in an uptrend without pressure to correct at the moment.

Pin Action in the SL Portfolio.

We are weary of the finance sectors giving then taking away. While it goes against the idea of diversification, we pulled out of all of our bank stocks. We got out of BOH with a 5.1% gain and left ZION with a 14.4% gain. We looked at the high volume days and they were not in the correct direction. We can do better with the money.

We closed out our position on MCD. We have had it almost a year and were in and out several times. It looks like our net was close to 2.3% since February 2010 plus some nice dividends. With dividends, it was 2.9%. Not what you would call spectacular.

Even though it was only about 6 weeks ago that we pimped PFE Pfizer, we looked at it early this morning and did not like what we saw in the volume and the direction. We are out with a 9.5% gain in 6 weeks. Please keep in mind that we are making some of these decisions on a cash need basis and a revaluation of our holding based more on EPSG and institutional market volume.

We still like the pharm sector and went with our pick of the day from yesterday WCRX Warner Chicolt. We are in at $23.83. We are looking for 30 by summer and have a stop set at $22.00.

And we added to our IBM position based upon some nice trending in the chart and positive volume. Look at the chart for 25th 28th and 1st of Feb to see what I mean. This puts our average cost at $145.26 giving us an unrealized gain of just under 13%. We are looking for 175-177 by summer. Our stop is in at $150.

Who are you Picking? I thought it woul be fun to close with a straw pole of who or readers are chosing for the Superbowl. I might take a night off of publishing tomorrow so I have chosen to send this out tonight. Send me your pick at brian.cronin@padi.com

Salve Lucrum

BIDI Baidu, Inc. provides Chinese and Japanese language Internet search services. Its search services enable users to find relevant information online, including Web pages, news, images, multimedia files, and blogs through the links provided on its Websites. If that description sounds familiar, that is because the business model is almost identical to GOOG Google Inc. In fact BIDU got a huge boost and a real solid foundation when GOOG chose to back step a bit in China. Before and since BIDU has been white hot. So that means we all lost a chance to get into the Chinese version of Google. Darn. BIDU is way too expensive with crazy P/E ratios. The current is 98 and forward looking is 50. When the S & P 500 is about 15-16, you gotta be crazy. Forget about it. Even the chart looks to hot to handle.

DO YOUR HOMEWORK. BIDU might be the next Google. $1,000 bucks in Google in 2004 (about the time its stock tracked BIDU) would be worth $5,545. The end point here is to not let the P/E ratio and current price scare you if you think the stock has legs.

IBD loves the stock and rates it a 98. Average earnings growth for the last three quarters is 139%. Year on year for the latest quarter is 109%. They beat expectations (BIG Expectations) by 13%. They have had 4 years of consecutive earnings growth and that was competing with Google. Google is all but gone from the market. It is performing in the top 5% of all stocks measured by IBD. It accumulating is neutral at the moment, but that might be because a lot of the big players (hedge fund, insurance companies etc,) were in and had to take some profit in December. If we see a few more days like Feb 1 you’ll see the accum/dist rating improve. 22 million shares were traded on Tuesday. Lost of new big traders. That’s a good thing. Let’s keep it close on a watch list.

Turning Over Some Stone

I have to admit we were tickled today to have one of our readers ask about a stock they were looking at. We were tickled as we admire this person’s knowledge and experience in the industry of financial advising. It was quite flattering. Thank you Doug.

The request was to kick the tires on RST Rosetta Stone Inc. which provides technology-based language learning solutions worldwide. The company develops, markets, and sells language learning solutions, such as software, online services, and audio practice tools primarily under the Rosetta Stone brand name. It offers self-study language learning solutions in approximately 31 languages. The company's approach, called Dynamic Immersion, eliminates translation and grammar explanation and is designed to leverage the natural language learning ability that children use to learn their native language. It also provides Rosetta Stone TOTALe, an online language learning solution that integrates its online courses with coach-led practice sessions, fun and engaging language games, interaction with native speakers, and live support from customer service agents. In addition, the company offers an online peer-to-peer practice environment called SharedTalk, at www.sharedtalk.com, where registered language learners meet for language exchange to practice their foreign language skills. It primarily serves individuals, home school parents, educational institutions, armed forces, government agencies, corporations, and not-for-profit institutions. The company sells its products through direct sales channels, including its call centers, Web sites, institutional sales force, kiosks, and certain retailers, as well as through the sale of CD-ROM's and on line subscriptions. Rosetta Stone Inc. is headquartered in Arlington, Virginia.

WE DO NOT OWN THE STOCK. We did have it on a watch list back in August, but never got a good entry point and forgot about it. Let’s look at the fundies first.

For the positive, they and analysts are looking for a 39% increase in earnings this year. They have about 5 bucks a share cash and decent cash flow. Institutional ownership seems to be slipping a bit. There are some target prices at 22 a share creating a fairly good margin of safety as the stock closed today at $19.38. On the down side, earnings did drop this year from last. The stock is trading below its 20, 50 and 100 day level. Considering the uptrend the market has had since August-September, RST seems to be going against the grain and seeking lower lows. Below is a chart that demonstrates is. Every singe volume day above the daily average has been a down day. As you know, in order to break over the average volume it takes institutional monies. This is also illustrated with the institutional ownership report we borrowed from Morningstar. You cans see the big money trends and they ain’t that pretty.

IBD does not like the pick. It has a 14 out of 99 overall rating on the equity. Most of the redflags include the sector rating which is educational software and is listed 116 out of 197 sectors. Most of the EPSG (Earnings per Share Growth) numbers were not impressive. It is 30% off its 52 week high and IBD likes stocks to at or near their 52 week high. The real negative for me is the IBD Accum/Dist rating. It is a D- which means this is being dumped. Being dumped in an upward market is not a good sign. Now let’s go to the SEC Filings and see if the CEO and CFO can tell why they are struggling.

In looking at the Nov 10Q filing, there are no surprises there and no real explanation other than 43% revenue comes directly from consumers and 30% comes from government and schools. Although it does not say it, the product is truly discretionary to the 43% base of consumers. In this day and age there are free and less expensive on line language learning aides and travel is just now beginning to recover. And as far as sales to the government and schools well good luck with that and be real careful of the accounts receivable. California is paying vendors with IOUs.

In a nutshell Rosetta has a great brand and plenty of opportunity. They generate less than 10 % of their revenue outside the US which leaves a lot of opportunity for growth, but they are not seeing it yet. They are well positioned in the largest brick and mortar and on line retailers in the world. That 30 % government business is leading to more international take up with other countries governments. The product itself is very effective and they have some proprietary technology with widens the competitive moat. All that said, we would wait until we see a reversal of institutional monies. RST needs a good quarter or two of earnings growth and few MF or Hedge funds to take notice and start accumulating. Until that happens, you are trying to catch a falling knife.

What happened today.

Now what actually did happened today in the market? We are batting about 60% on our data points and earnings calls this week which gives us some bragging rites. Snow Day In Manhattan. Ok they did not close banks and schools, but wicked weather made it hard to get buys and sellers together so volume was light and the number went sideways. The good news is we are still in an uptrend without pressure to correct at the moment.

Pin Action in the SL Portfolio.

We are weary of the finance sectors giving then taking away. While it goes against the idea of diversification, we pulled out of all of our bank stocks. We got out of BOH with a 5.1% gain and left ZION with a 14.4% gain. We looked at the high volume days and they were not in the correct direction. We can do better with the money.

We closed out our position on MCD. We have had it almost a year and were in and out several times. It looks like our net was close to 2.3% since February 2010 plus some nice dividends. With dividends, it was 2.9%. Not what you would call spectacular.

Even though it was only about 6 weeks ago that we pimped PFE Pfizer, we looked at it early this morning and did not like what we saw in the volume and the direction. We are out with a 9.5% gain in 6 weeks. Please keep in mind that we are making some of these decisions on a cash need basis and a revaluation of our holding based more on EPSG and institutional market volume.

We still like the pharm sector and went with our pick of the day from yesterday WCRX Warner Chicolt. We are in at $23.83. We are looking for 30 by summer and have a stop set at $22.00.

And we added to our IBM position based upon some nice trending in the chart and positive volume. Look at the chart for 25th 28th and 1st of Feb to see what I mean. This puts our average cost at $145.26 giving us an unrealized gain of just under 13%. We are looking for 175-177 by summer. Our stop is in at $150.

Who are you Picking? I thought it woul be fun to close with a straw pole of who or readers are chosing for the Superbowl. I might take a night off of publishing tomorrow so I have chosen to send this out tonight. Send me your pick at brian.cronin@padi.com

Salve Lucrum

posted by J.J. Phineaus at 10:35 PM

![]()

![]()

0 Comments:

Post a Comment

<< Home